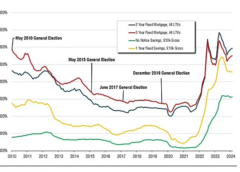

The Bank of England held its Bank Rate at 5.25% in May, as was widely expected. It was the sixth time in a row the Rate has been frozen since it rose to its current level in August last year. The Rate had previously undergone 14 consecutive rises (between December 2021, when it stood at just 0.1%, and last August).

The next interest rate announcement by the Bank’s Monetary Policy Committee (MPC) will be tomorrow, 20 June. The European Central Bank cut interest rates on 6 June which, in theory, could make a cut from the Bank of England more likely. But the general election on 4 July may delay any cut until the MPC’s next meeting in August.

Read More